The Fast Company Impact Council is an invitation-only membership community of leaders, experts, executives, and entrepreneurs who share their insights with our audience. Members pay annual dues for access to peer learning, thought leadership opportunities, events and more.

“Every accumulation becomes the means of new accumulation.” This is what Karl Marx has to say about capital. He does not get enough credit for being one of the more accurate predictors of capitalism because people understandably do not like his solution. But the truth is, most philosophers do not even present a solution and he understood the problem as well as anyone.

We saw more bankruptcies in 2024 than in the last 14 years, and consumer discretionary was the leading bankruptcy sector. This problem will only increase as AI proliferates. And while the linked article cites other reasons, we think the larger reason is Amazon. Amazon has achieved a level of automation and scale through what can only be described as accelerating accumulation. This is the major reason brick and mortar retail has become so tough, and Amazon’s control of the supply chain makes it harder for online businesses to compete. But why do we think this is just the beginning?

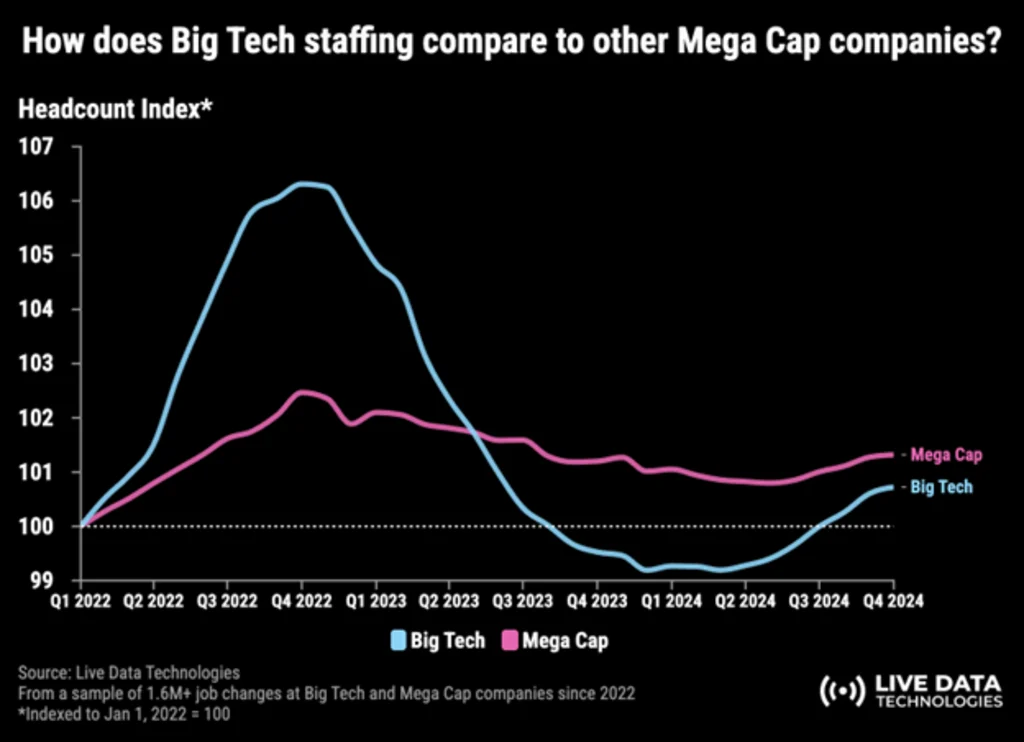

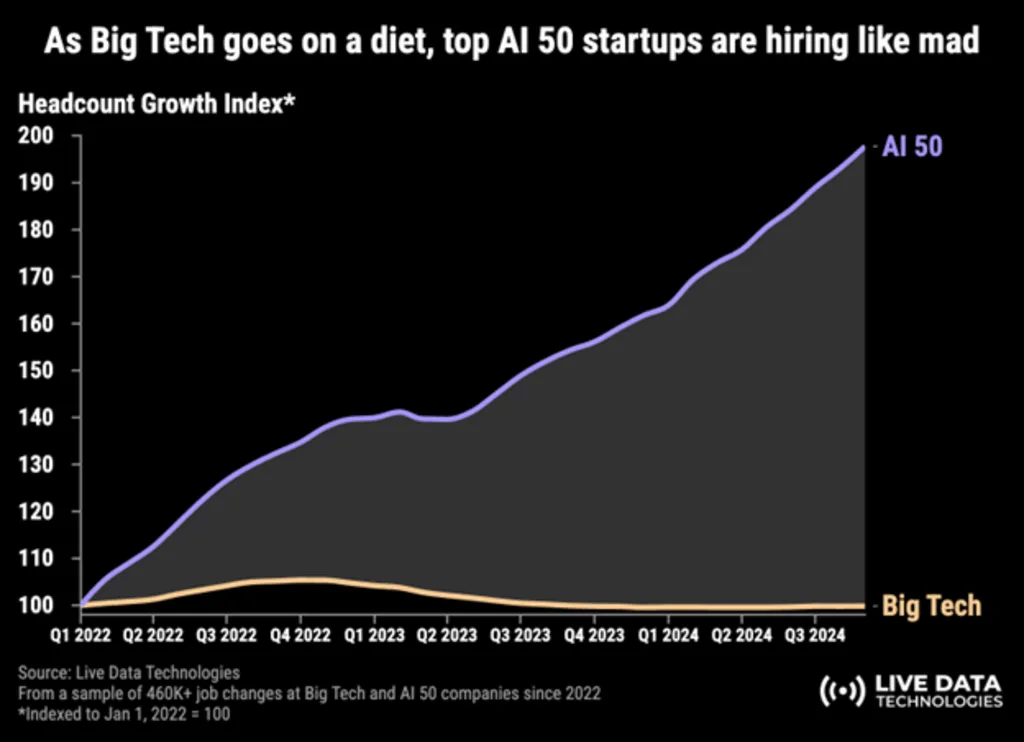

We are seeing a clear increase in funding and headcount towards AI. Eighty-seven percent of Y Combinator’s latest batch of companies focus on AI—a huge sign we are only scratching the surface of a move towards automation that can threaten small businesses. Soon it will not just be smaller businesses in the consumer cyclical sector threatened by this concerted push towards automation. But it is not just the startup world seeing this trend. Even our most successful companies are slowing down their hiring; at the same time the top 50 AI startups are accelerating at close to a 200% rate.

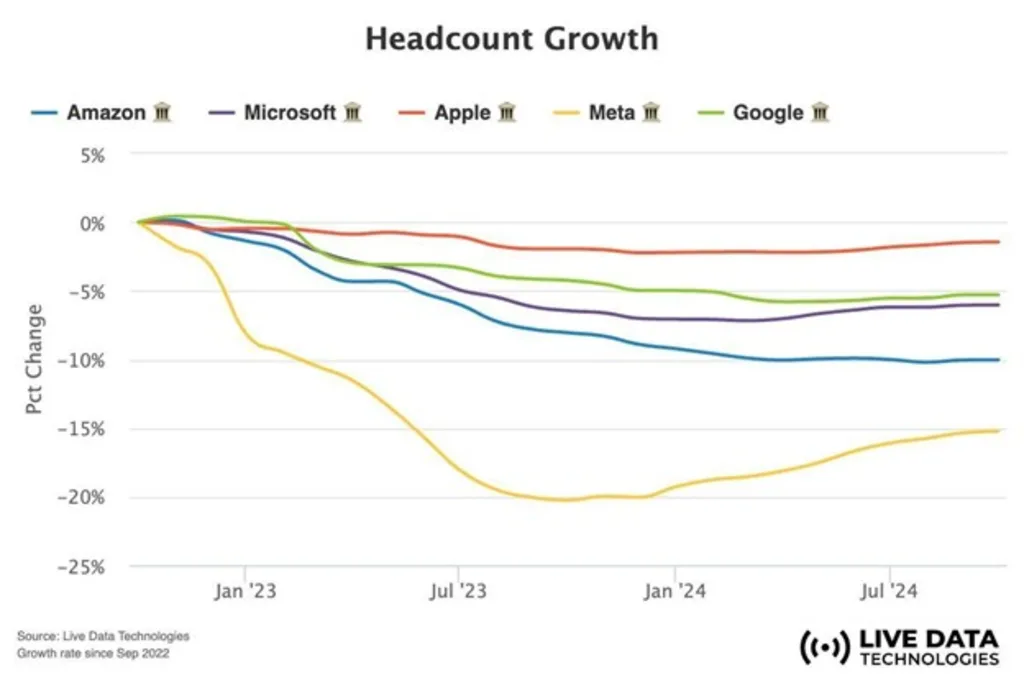

Big tech hiring slows

Live Data Technologies on Big Tech Headcount Growth

Contrasting Magnificent Seven companies that lean on AI versus more pure AI plays in the AI 50, you can see the scary trend towards more complete automation. Larger commitments to automation could further acceleration reduction in headcount, especially for engineering positions. Google recently announced that over 25% of its code was written by AI. If some of the most talented engineers in the world at Google can no longer compete with their AI, how much longer do small and medium sized businesses have before, at the very least, their funding environment becomes more difficult as a result, and bankruptcy ensues?

Traditionally, small caps have lower profitability but higher growth potential, while large caps are the opposite. But here’s what our data found: Companies with a profitability score above 90, typically large or mega caps, are now growing at nearly the same rate as small caps. It’s not just a statistical fluke. This pattern has only emerged during past industrial revolutions, when large companies leveraged new technologies, from railroads to oil, to dominate markets. Today, AI is the catalyst, and it’s the big players like Nvidia that are reaping the benefits.

What is even more alarming about these numbers is those of the largest companies. Stocks in the 90th percentile or above in Prospero.ai’s profitability rating are growing more than 80%. This is strong evidence that even the most profitable companies are not being slowed down by their size. Generally it is easier to grow at faster rates if your company is less mature from a profitability standpoint. The fact that the smallest companies < 10 are also projected to grow at slower rates than <20 is perhaps even more shocking. Companies with the smallest revenue should have the easiest time growing at a faster rate. Moving from $1 million in revenue to $2 million from one year to the next is easier than going from, say, $25 million to $50 million.

Profit fuels growth

If you are looking for the flagship demonstration of this idea, look no further than Nvidia. It generates billions of dollars in profit each quarter, while still achieving massive growth. Revenue from fiscal 2025 was up 114%. Looking for a benchmark number led us to Amazon, one of the greatest growth stories of our time. Amazon posted 60.52% growth when comparing Q4 2024 and Q4 2023 quarterly operating income, and posted its best quarter in the last 15 years. And it did that at roughly half of Nvidia’s revenue.

That is what makes the Nvidia story so interesting. In 2023, Nvidia had a 98% market share in data center GPUs. Other domestic and international companies have been trying to compete with them in this market, and they simply cannot. Nvidia’s financial strength allows it to attract the best talent and develop cutting-edge AI technologies, creating a cycle where profit fuels growth, which then drives more profit.

Now what does this mean for small caps? I think the implications are pretty clear. We’re seeing the monopolization ramp up, just as we did in past revolutions. Large companies, flush with cash, have the means to capitalize on advantages of scale in ways that small players simply can’t match. This makes it harder and harder for small cap companies to compete on the type of growth metrics it takes to attract the needed capital to compete in ever more competitive spaces. The rich get richer, and the competitive gap widens.

So, what’s the bottom line? AI-driven bankruptcy isn’t just a matter of companies failing; it’s a symptom of an economic shift where capital accumulation accelerates faster than ever before. This isn’t just a chapter in bankruptcy law, it’s a chapter in how AI will redefine capitalism itself.

George Kailas is CEO of Prospero.Ai.